5 Things to Check Before Signing a Commercial Lease

Renting a new workspace is a massive milestone for your growing company. Getting the keys to a fresh office, retail store, or warehouse feels like a major victory. However, signing a commercial lease agreement requires serious attention to detail.

Unlike residential leases, commercial contracts offer far less legal protection for the tenant. The rules are stricter, the financial commitments are larger, and the terms are often heavily weighted in favor of the landlord. Failing to read the fine print can lock your company into a restrictive, expensive rental agreement for years.

To help you protect your business and secure a fair deal, here is exactly what you need to review before putting pen to paper.

Insights from Real Estate Developers Dubai

If you are expanding internationally or looking at global hubs, you might encounter properties built by major Real Estate Developers Dubai. These developers frequently offer premium, state-of-the-art commercial spaces. However, their contracts often include highly specific clauses regarding property modifications, service charges, and community fees. Even if you are operating locally, understanding how premium developers structure their leases gives you a great baseline for what to expect in high-end commercial property markets. Always review the specific building rules, as they can directly impact how you run your daily operations.

Why Hire a professional business development consultant

Navigating complex legal documents is rarely a simple task. Bringing a professional business development consultant onto your team can save you thousands of dollars. These experts understand the local market conditions and know exactly what standard lease terms look like. They can easily spot unfavorable clauses, help you negotiate better rates, and ensure the contract aligns perfectly with your long-term growth strategy. Having an expert in your corner gives you the confidence to negotiate effectively.

1. Scrutinize the Lease Terms and Duration

The very first thing to verify is the exact length of the lease. Are you signing a three-year, five-year, or ten-year agreement? You need to ensure the timeline matches your business projections.

A short-term lease offers flexibility if you outgrow the space quickly, but it might come with a higher monthly base rent. A long-term lease locks in your rate and provides stability, but it can be a financial burden if your business faces unexpected challenges. Additionally, check for renewal options. You want the right to renew your lease at a predetermined, fair rate before the landlord puts the space back on the open market.

2. Look Out for Hidden Costs

In a commercial lease, your monthly base rent is usually just the starting point. Many landlords use a Triple Net Lease (NNN) structure. This means the tenant is responsible for paying the base rent, plus a share of the property taxes, building insurance, and Common Area Maintenance (CAM) fees.

Take a close look at how CAM fees are calculated. These charges cover the maintenance of shared spaces like lobbies, elevators, and parking lots. Ask the landlord for a breakdown of past CAM charges to get a realistic estimate of your total monthly expenses. Identifying these hidden costs early prevents budget blowouts later on.

3. Understand Tenant Obligations for Maintenance

When a pipe bursts or the air conditioning breaks down, who pays for the repairs? In residential renting, the landlord handles almost everything. In commercial real estate, tenant obligations are usually much higher.

Your lease should clearly define the maintenance responsibilities of both parties. Typically, the landlord handles the structural elements of the building, such as the roof and exterior walls. The tenant is often responsible for the interior plumbing, electrical systems, and HVAC (heating, ventilation, and air conditioning) maintenance. Make sure the HVAC unit is inspected and in good working condition before you sign, so you do not inherit an expensive repair bill on day one.

4. Check the Termination Clause

Sometimes, things simply do not work out. You might need to relocate, downsize, or close up shop entirely. It is crucial to understand what happens if you need to break the lease early.

Review the termination clause thoroughly. Does the landlord require a massive penalty fee for early exit? Do you have the option to sublease the space to another business? A subletting clause can be a financial lifesaver if you need to move out before your term expires. Negotiate for the right to sublet or assign the lease, ensuring you have an escape route if your business circumstances change dramatically.

5. Review the Permitted Use Clause

Landlords want to control exactly what happens on their property. The permitted use clause dictates exactly what type of business activities you can conduct in the space.

If the clause is written too narrowly, it could restrict your ability to expand your services in the future. For example, if you rent a space for a “coffee shop,” you might be blocked from selling hot food or merchandise later on. Try to negotiate a broad permitted use clause. Use language like “any lawful retail business” rather than hyper-specific descriptions.

Helpful Tips for Negotiating Your Lease

- Hire a commercial real estate attorney: Never rely solely on the landlord’s agent. Have a lawyer review every page of the document.

- Ask for a rent-free fit-out period: If the space requires significant renovations before you can open your doors, ask for one or two months of free rent to cover your construction time.

- Document the initial condition: Before you move in, take detailed photos and videos of the space. This protects your security deposit when it is time to move out.

- Negotiate a co-tenancy clause: If you rely on foot traffic from an anchor tenant (like a major grocery store in a shopping plaza), a co-tenancy clause allows you to break your lease or pay reduced rent if that anchor tenant leaves.

Frequently Asked Questions

What is a personal guarantee in a commercial lease?

A personal guarantee means that if your business fails and cannot pay the rent, you are personally liable for the debt. Landlords often require this for new businesses. Try to negotiate a time limit on the guarantee, such as for the first two years of the lease only.

Can my landlord arbitrarily raise the rent?

Not if your lease includes a fixed rent escalation clause. This clause outlines exactly when and by how much your rent will increase (usually an annual percentage). Always review this to ensure the increases are tied to a fair metric, like the Consumer Price Index (CPI).

What is a letter of intent (LOI)?

An LOI is a preliminary, non-binding document outlining the basic terms of the lease. It shows the landlord you are serious and sets the foundation for drafting the final, legally binding commercial lease agreement.

Final Words on Securing Your Workspace

Signing a commercial lease agreement is a significant commitment that will impact your bottom line for years to come. By taking the time to thoroughly review the lease terms, identify hidden costs, and clarify your tenant obligations, you protect your company’s future. Do not be afraid to negotiate aggressively and bring in professionals to review the paperwork. A well-negotiated rental agreement sets the perfect foundation for your business to thrive in its new home.

Related Posts

How Market Cap Affects Shareholder Value

Understanding how the market assesses a company’s worth provides insight into how investors interact with its stock. This measure changes continuously as prices move and sentiment evolves, shaping perceptions of stability, growth prospects, and business strength. As shareholder interests are tied to these movements, changes in valuation influence how investor

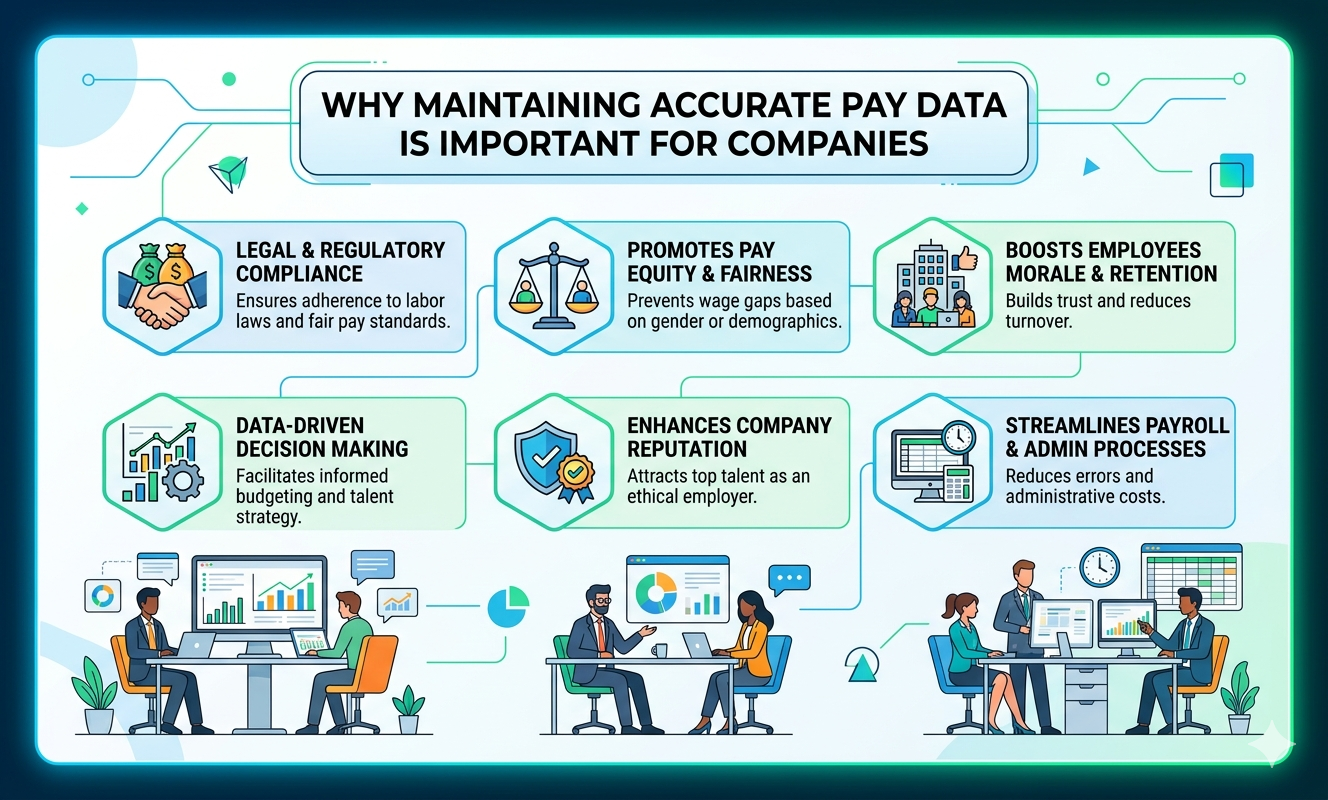

Why Maintaining Accurate Pay Data Is Important for Companies

Accurate pay data is the foundation of a reliable payroll system. Every company, whether small or large, depends on precise financial records to ensure employees receive the correct compensation and to maintain compliance with legal standards. When businesses prioritize accuracy in payroll, they build trust, avoid costly errors, and support long-term growth. To

Fast and Trusted Mobile Repair in Dunoon by Experts

If your phone stops working, it can ruin your whole day. People use their phones for calls, messages, work, and even banking. That is why finding the right mobile repair in Dunoon is very important. A good repair service can fix your phone fast and save you money. At Ayr Phone Repair Shop, we understand how important your device is. Our team works hard to give

Fast, Safe & Reliable ADHD Support: Why Patients Choose to Buy Adderall Online

Managing Attention Deficit Hyperactivity Disorder (ADHD) requires a structured approach that combines medical guidance, behavioral support, and effective medication. One of the most widely prescribed treatments is Adderall, a proven solution that helps improve focus, reduce hyperactivity, and enhance impulse control. Today, many individuals prefer to buy addera

Leave a Reply